For residential rental properties purchased after 27 March 2021 that are not new builds, you will not be able to claim any interest deductions.

Interest incurred on a new build that is bought for investment purposes is still able to be claimed as an interest deduction. There is limited detail on what qualifies for a new build, although it appears to include properties that are acquired within a year of the Code Compliance Certificate being issued.

From 1 October 2021, residential property investors who own an existing rental property will also be restricted to the amount of interest they can claim as a deductible expense.

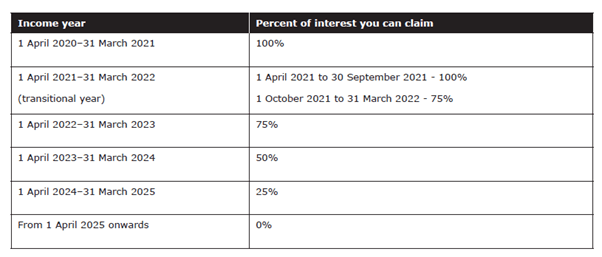

Interest deductibility on residential rental properties will be phased out over the next four year, so that by 1 April 2025 there be no interest claims. The phase sees interest deductibility reducing each financial year as outlined in the table below:

How may this affect you?

You may be receiving $25,000 per year in rent, and pay $5,000 in rates, insurance, and repairs, and $20,000 in interest. Currently, you would have no profit for the year because your expenses are the same as rental income.

Now, (after the new rule is phased in) you will have to pay tax (~$6,600 at a 33% rate) on $20,000 of interest costs, due to the interest cost not being a deductible expense. Net cashflow will be negative $6,600 due to the new tax rules, when previously it was neutral (prior to any mortgage principal repayments).

The government has also announced changes to extend the bright line test. Read further here.

Contact Us

Contact Tim Doyle or Jane Evans today to discuss your business continuity planning needs (or any other matter) on 07 823 4980 or email us. Our office is in Cambridge, NZ, but distance is no problem. We have many international and national clients.

This material has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for, tax, legal or accounting advice. You should consult your own tax, legal and accounting advisors before engaging in any transaction.